Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Are You Better Off Paying Your Mortgage Earlier or Investing Your Money?

Posted in Buying, Selling, and Living by Guest Author

Photo Credit: Rawpixel via Unsplash

Few topics cause more division among economists than the age-old debate of whether you’re better off paying off your mortgage earlier, or investing that money instead. And there’s a good reason why that debate continues; both sides make compelling arguments.

For many people, their mortgage is the largest expense they will ever incur in their lives. So if given the chance, it only makes logical sense you would want to pay it off as quickly as possible. On the other hand, a mortgage is also the cheapest money you will ever borrow, and it’s generally considered good debt. Any extra money you obtain could be definitely be put to good use elsewhere.

The reality is, however, a little less cut and clear. For some homeowners, paying off their mortgage earlier is the right answer. While for others, it would be far more advantageous to invest their money.

Advantages of paying off your mortgage earlier

- You’ll pay less interest: Each time you make a mortgage payment, a portion is dedicated towards interest, and another towards principal (we’ll ignore other costs for now). Interest is calculated monthly by taking your remaining balance, the length of your amortization period, and the interest rate agreed upon with your lending institution.

If you have a $300,000 mortgage, at a 4% fixed rate over 30 years, your monthly payment would be around $1,432.25. By the time you finish paying off your mortgage, you would have paid a total of $515,609, of which $215,609 were interest.

If you wanted to lower the total amount you pay on interest, you don’t need to make a large lump sum to make a difference. If you were to increase your monthly mortgage payment to $1,632.25 (a $200 a month increase), you would be saving $50,298 in interest, and you’ll pay off your mortgage 6 years and 3 months earlier.

Though this is an oversimplified example, it shows how even a small increase in monthly payments makes a big difference in the long run.

- Every additional dollar towards your principal has a guaranteed return on investment: Every additional payment you make towards your mortgage has a direct effect in lowering the amount you pay in interest. In fact, each additional payment is, in fact, an investment. And unlike stocks, bonds, and other investment vehicles, you are guaranteed to have a return on your investment.

- Enforced discipline: It takes real commitment to invest your money wisely each month instead of spending it elsewhere.

Your monthly mortgage payments are a form of enforced discipline since you know you can’t afford to miss them. It’s far easier to set a higher monthly payment towards your mortgage and stick to it than making regular investments on your own.

Besides, once your home is completely paid off, you can dedicate a larger portion of your income towards investments, your children or grandchildren’s education, or simply cut down on your working hours.

Advantages of investing your money

- A greater return on your investment: The biggest reason why you should invest your money instead comes down to a simple, green truth: there’s more money to be made in investments.

Suppose that instead of dedicating an additional $200 towards your monthly mortgage payment, you decide to invest it in a conservative index fund which tracks S&P 500’s index. You start your investment today with $200 and add an additional $200 each month for the next 30 years. By the end of the term, if the index fund had a modest yield of 5% per year, you will have earned $91,739 in interest, and the total value of your investment would be $163,939.

If you think that 5% per year is a little too optimistic, all we have to do is see the S&P 500 performance between December 2002 and December 2012, which averaged an annual yield of 7.10%.

- A greater level of diversification: Real estate has historically been one of the safest vehicles of investment available, but it’s still subject to market forces and changes in government policies. The forces that affect the stock and bonds markets are not always the same that affect real estate, because the former are subject to their issuer’s economic performance, while property values could change due to local events.

By putting your extra money towards investments, you are diversifying your investment portfolio and spreading out your risk. If you are relying exclusively on the value of your home, you are in essence putting all your eggs in one basket.

- Greater liquidity: Homes are a great investment, but it takes time to sell a home even in the best of circumstances. So if you need emergency funds now, it’s a lot easier to sell stocks and bonds than a home.

Misael Lizarraga is a real estate writer with a passion for teaching real estate concepts to first time buyers and investors. He runs realestatecontentguy.com and is a contributing writer for several leading real estate blogs in North America.

A History Lesson

One of the most common questions we hear from clients is “Where do you think interest rates are going?”

One of the most common questions we hear from clients is “Where do you think interest rates are going?”

Virtually all of the experts we follow put rates above 5% going into next year and some see rates approaching 5.5% by the middle of 2019. What’s certain is that there are economic forces at work that are pushing rates higher.

So, how about a little history lesson? How do today’s 30- year mortgage rates compare to this same date in history going all the way back to 1990?

• Today = 4.85%

• 2017 = 3.94%

• 2015 = 3.82%

• 2010 = 4.27%

• 2005 = 5.98%

• 2000 = 7.84%

• 1995 = 7.75%

• 1990 = 10.22%

While today’s rates feel high only because they are higher than 2017, they are quite a bit lower than at many times in history.

A Beginner’s Guide to Securing a Mortgage Loan

![]()

Entering into debt is a concept I grew up diametrically opposed to. I was raised, like many with frugal family members, to understand that anything you couldn’t pay for on the spot was something you couldn’t afford. But as we age we learn the pathway to financial growth requires a commitment beyond what many of us can deliver up front. Building and stabilizing wealth is, for many families, tied to home ownership. To reach that initial threshold, most aspiring homeowners will need to apply for a mortgage loan. That process can be daunting, but the long-term rewards of securing your home are worth it.

Step One – Break down your budget

A major financial decision like this can’t be made lightly. Many experts recommend a 50-20-30 style plan for finances, particularly for first-time homeowners. That means 50% of your budget is committed to core, unavoidable, monthly expenses like rent, groceries, loan payments, utilities, insurance, etc. The 20% segment is savings, placed in reserve towards a general or specific future financial goal. The final 30% (at maximum) is left as a remainder for personal spending, however, is most desired. Once this is set, you’re ready to evaluate the rate at which you can repay your loan and adjust accordingly.

Step Two – Take the time to get it right

It’s exciting to be in a position to purchase your first home, but if you find the right spot and realize the funds aren’t there yet it can be a huge disappointment. That’s what makes seeking pre-approval for a loan a must – particularly if it’s your first time. Having your credit in order, along with all key financial documentation (bank statements, tax returns, debt copies, prior records of significant ownership). If your credit isn’t in a great place, it’s likely worth taking the time to amend it before applying for your mortgage loan. When you earn lower interest rates and more manageable monthly payments you’ll be thankful for your prudence.

Step Three – The bigger the down payment the better

It’s rare that first-time homebuyers have significant cash on hand, but whatever you can muster makes a difference. Typically, the greater a down payment you can muster, the lower your subsequent interest rates will be. For many, there’s only so much that’s tenable as a bulk sum up front, of course. If that fits your situation, seeking a loan insured by the Federal Housing Administration (FHA) can earn you a healthy loan for a down payment of just 3.5% of your home’s total value. To calculate the limitations of your target home’s loan options, you can input your information on the Department of Housing and Urban Development (HUD) website here.

Step Four – Stick to the plan!

After all the effort you’ll go through to secure a mortgage loan, you’ve earned the home it’s helped you purchase. That loan, like any loan, is contingent on your continued monthly payments. It can feel daunting and dispiriting after a time to continually be paying for a home you’re already living in, but maintaining your financial balance is vital. You’ll never be able to predict every expense that comes up but maintaining your budget towards paying off your mortgage loans will set you up to be more financially flexible in the future. Should you ever hope to purchase a second home or other major investments requiring of loans, having a record of consistent mortgage loan payment can help you secure far more favorable interest rates in the future.

A mortgage loan, like any loan, is a major commitment, but entering into homeownership is a massive step towards financial stability and future life-planning. With proper patience and focus, you can get the loan you need at the rate you can afford.

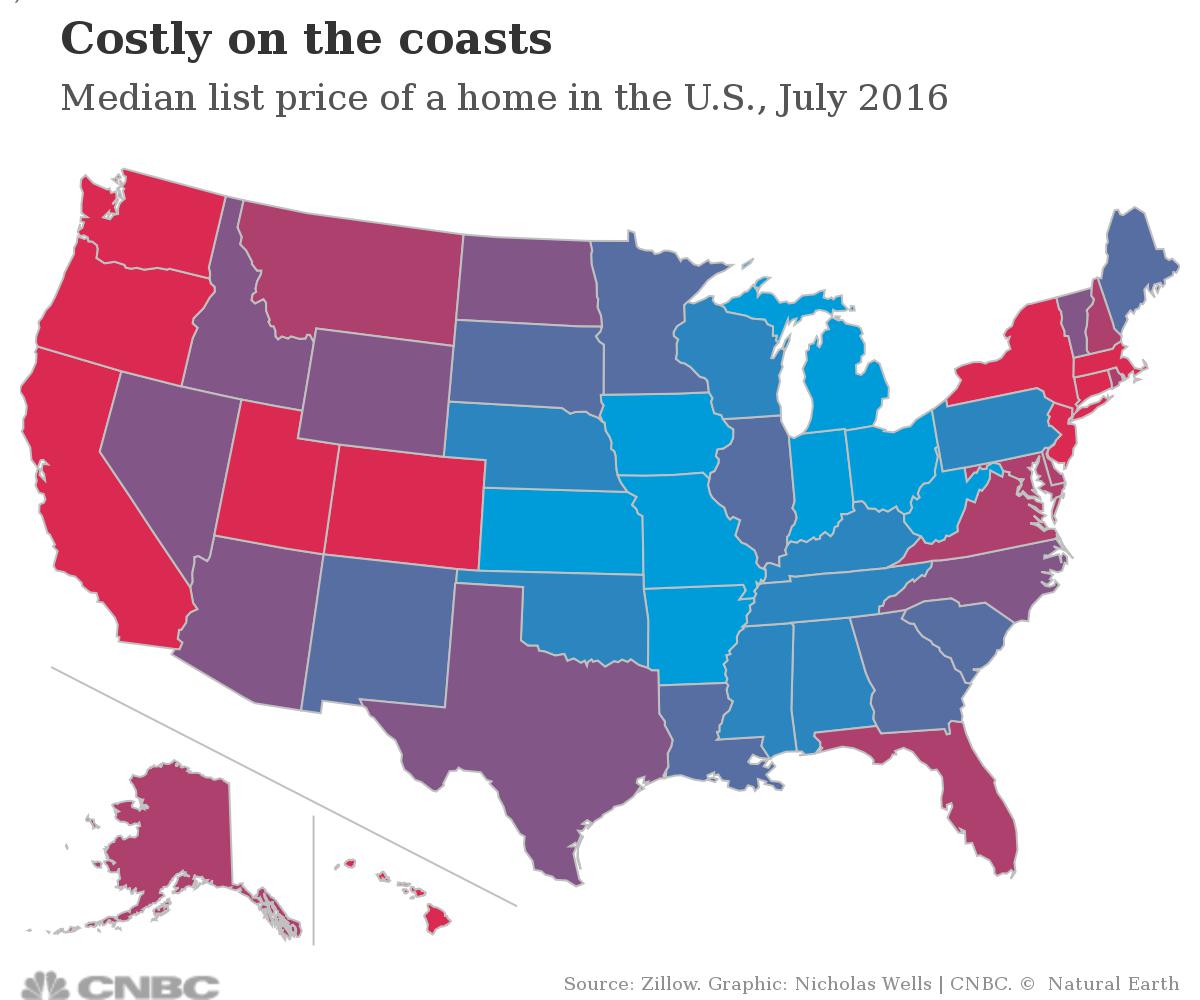

Limited Choices

Pretend that customer walks into our office and tells us they are looking for a single family home in Fort Collins. We would tell them that there  are 314 to choose from. But if they told us their price range is up to $300,000, their choices would be limited to just 10 homes.

are 314 to choose from. But if they told us their price range is up to $300,000, their choices would be limited to just 10 homes.

Our Crystal Ball

Last week Windermere’s Chief Economist Matthew Gardner joined us for our annual Market Forecast events in Colorado. We were pleased to host over 500 customers at two events in Denver and Fort Collins.

host over 500 customers at two events in Denver and Fort Collins.

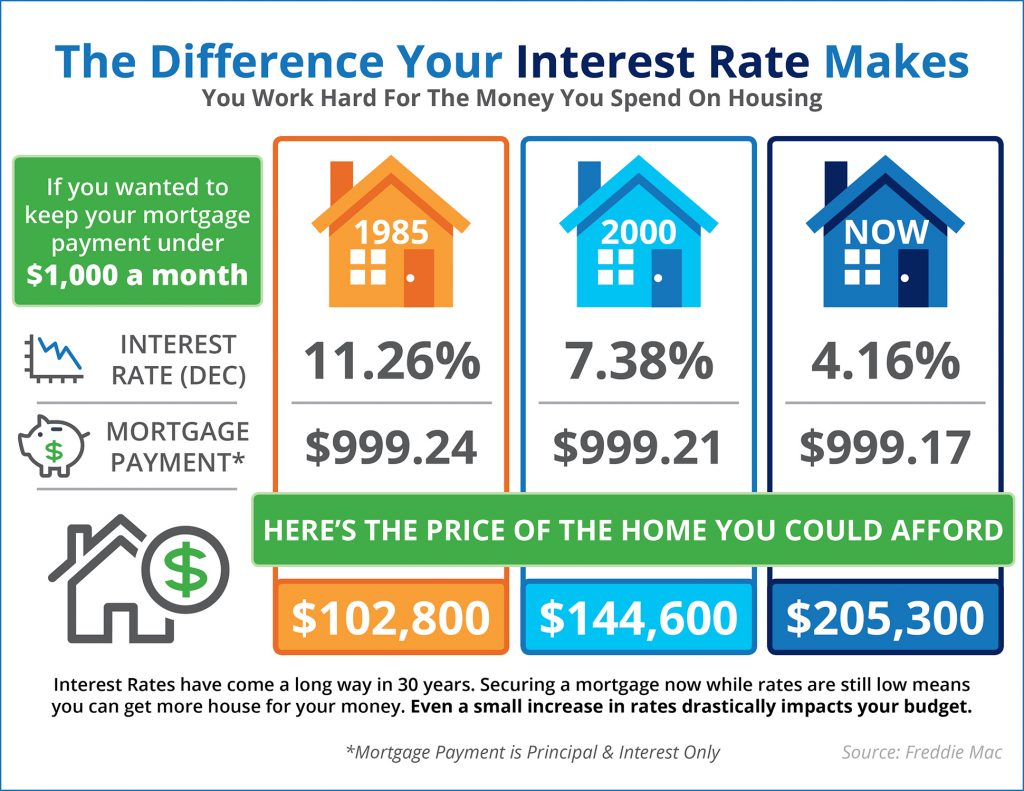

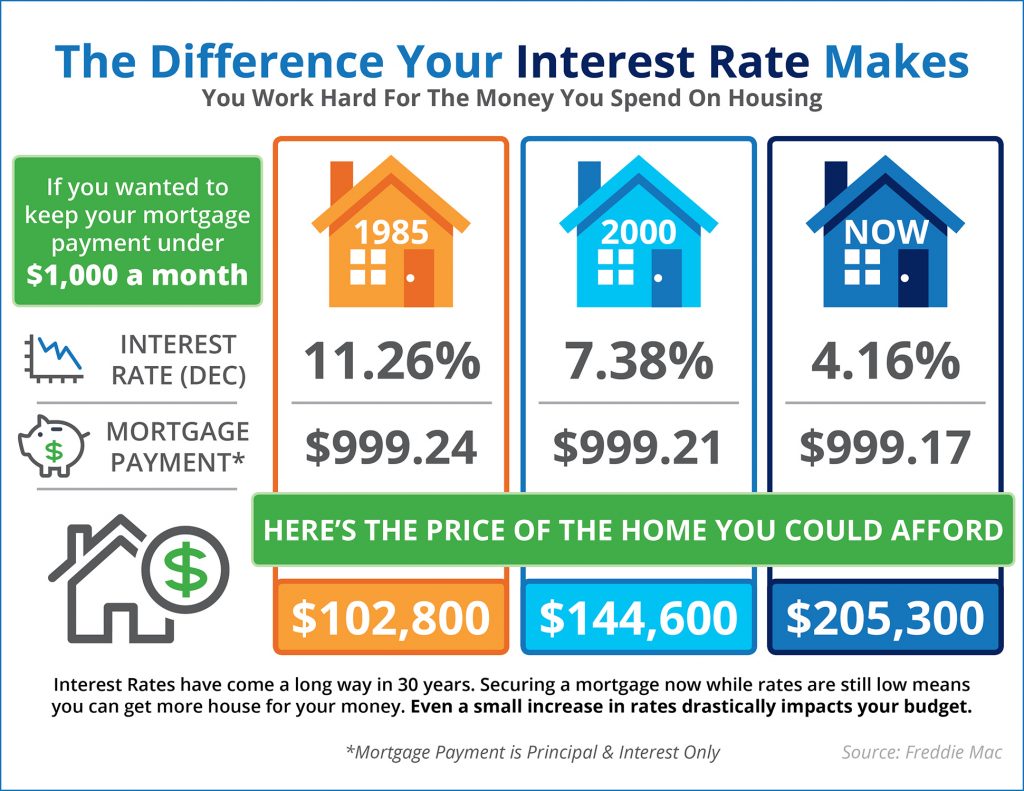

How Interest Rates Impact Your Buying Power

Know your risk. How will your buying power be impacted with increased interest rates?

Check out this infographic for an understanding of how much interest rates affect how much home you can afford.

Source: www.simplifyingthemarket.com Read the full article here: http://www.simplifyingthemarket.com/en/2016/12/16/the-impact-your-interest-rate-has-on-your-buying-power-infographic/?a=79696-9675764dc3b9cb63398c8d3c043b0717

100K

The City Manager for Fort Collins, Darin Atteberry, recently visited our weekly sales meeting. He had several interesting and valuable facts to share, including this…

Based on the City’s research, Fort Collins will grow by 100,000 people over the next 25 to 32 years. That will bring the population to approximately 255,000 people. It means Fort Collins will essentially add the equivalent of Boulder’s population over the next two and a half decades.

Based on the City’s research, Fort Collins will grow by 100,000 people over the next 25 to 32 years. That will bring the population to approximately 255,000 people. It means Fort Collins will essentially add the equivalent of Boulder’s population over the next two and a half decades.

The Trump Tantrum

Since the election interest rates have jumped from 3.77% to 3.95% according to the Mortgage Bankers Association.

Since the election interest rates have jumped from 3.77% to 3.95% according to the Mortgage Bankers Association.

“This week’s increase in mortgage rates, being dubbed the ‘Trump Tantrum,’ is the biggest one week increase since the ‘Taper Tantrum‘ in June 2013,” said Bankrate’s chief financial analyst Greg McBride.

Economists say the anticipation of Trump’s pledged spending plans and tax cuts have investors anticipating some inflation and a dose of adrenaline to the economy which have caused a great deal of volatility in the market.

A little perspective is in order- rates today are still lower than the 3.97% recorded last year at this time. And, rates today are still essentially half of their long-term average.

Using a $400,000 home as an example with a 20% down payment, this interest rate increase translates to an additional $34 per month.

Many economists believe that we are now seeing the beginning of a long-term rise in interest rates.

source: Inman News

Beware of Low Down Payments

First-time buyers can borrow with little down, but that may not be wise

Financial planners warn: "Borrowers should not overlook the true measure of home affordability: monthly cash flow."

Is your down payment going to affect your cash flow in the end? Check out this article to see what they suggest.

http://www.cnbc.com/2016/09/02/homebuyers-beware-of-banks-offering-too-much-cash.html