Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Q3 2021 Colorado Real Estate Market Update

The following analysis of the Metro Denver & Northern Colorado real estate market is provided by Windermere Real Estate Chief Economist Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact your Windermere Real Estate agent.

Regional Economic Overview

The rise in COVID-19 infections due to the Delta variant caused Colorado’s job recovery to slow, but not as much as in many other states. The latest data (for August) shows that more than 293,000 of the 376,000+ jobs that were shed due to COVID-19 have returned. This is good news, with only 83,000 jobs needed to return to pre-pandemic employment levels. The metro areas contained in this report have recovered 243,700 of the 310,000 jobs lost, and I expect the state will recover the remaining jobs by next summer. With employment levels improving, the state unemployment rate currently stands at 5.9%—down from the pandemic peak of 12.1%. Regionally, unemployment levels range from a low of 4.4% in Boulder to a high of 6.1% in Grand Junction.

__________

Colorado Home Sales

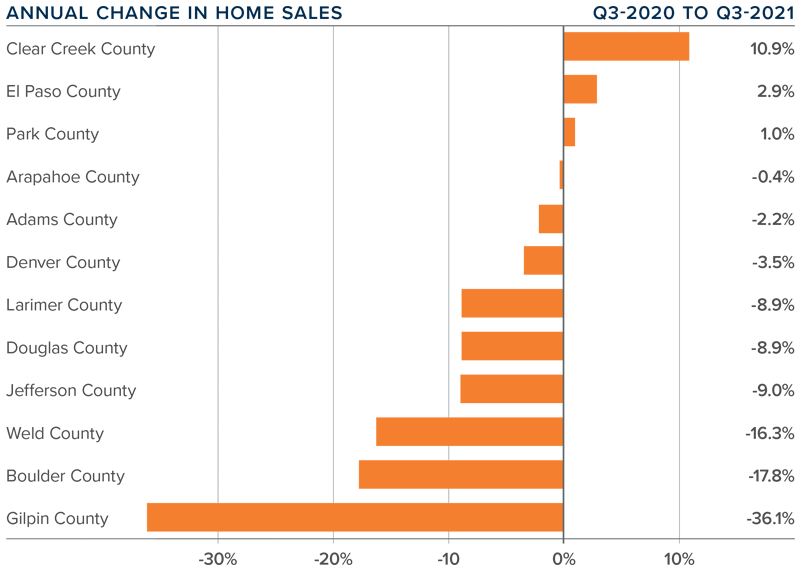

❱ Compared to a year ago, listing activity was down more than 30%. However, inventory levels were up 38.3% compared to the second quarter of this year, suggesting that buyers have more choice now than they have seen in some time.

❱ Although comparing current sales activity with that of a year ago is not that informative—given that the country was experiencing a massive rebound in housing demand following the outbreak of COVID-19—it was pleasing to see sales up in every county other than Denver and Douglas compared to the second quarter of this year.

❱ Pending sales (an indicator of future closings) were down 5.4% compared to the second quarter of the year, suggesting that closings in the final quarter may well be a little soft.

__________

Colorado Home Prices

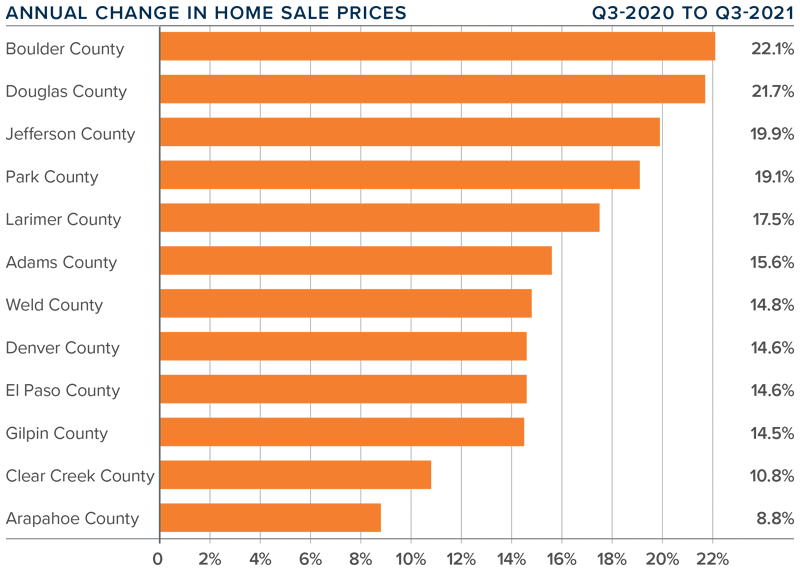

❱ Prices continue to appreciate at a very rapid pace, with the average sale price up 15.8% year over year to an average of $605,576. Sale prices were 1.6% lower than in the second quarter of 2021.

❱ Four counties—Arapahoe, Douglas, Weld, and Park—saw the average home sale price pull back between the second quarter and the third, but I am not overly concerned by this at the present time.

❱ Year-over-year, prices rose across all markets covered by this report. All counties except Arapahoe saw double-digit gains, but even that market saw an increase in sale prices.

❱ Several counties are experiencing a drop in average list prices, which is a leading indicator of future activity. As such, I expect to see the rise of sale prices start to slow, which will be a welcome sight for many buyers.

__________

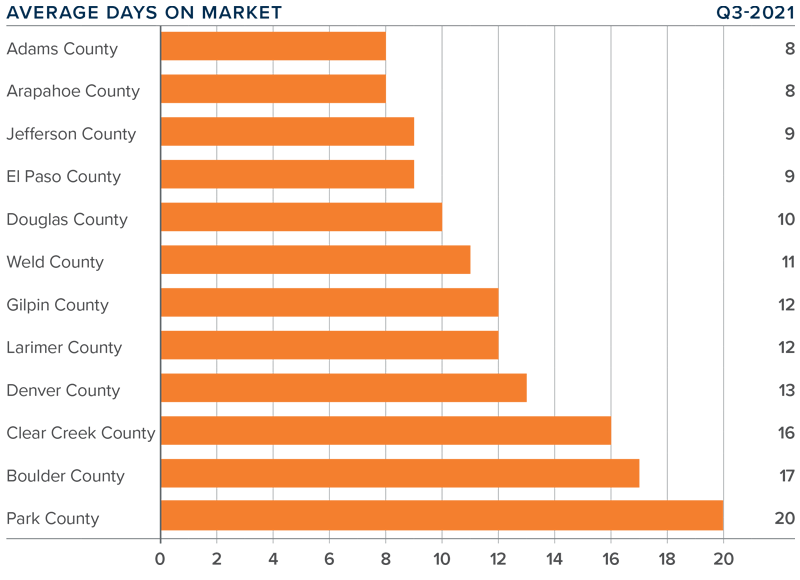

Days on Market

❱ The average number of days it took to sell a home in the markets contained in this report dropped 17 days compared to the third quarter of 2020.

❱ The length of time it took to sell a home dropped in every county contained in this report compared to both the same quarter a year ago and the second quarter of this year.

❱ It took an average of only 12 days to sell a home in the region, which is down 2 days compared to the second quarter of 2021.

❱ The Colorado housing market remains very tight as demonstrated by the fact that it took less than three weeks for homes to sell in all counties contained in this report.

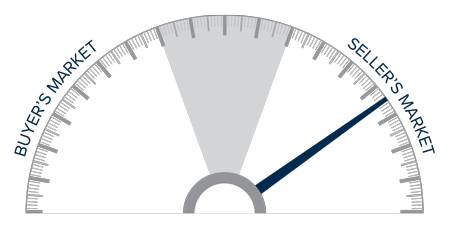

Conclusions

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

The job market continues to improve, which is always a stimulant when it comes to home buying. Inventory levels have improved, and lower pending sales suggest that buyers are taking a little longer to decide on a home. That said, the market is still bullish as indicated by the short length of time it took to sell a home in the quarter. Mortgage rates will start to creep higher as we move into the winter months, and this may stimulate additional buying activity. In the last edition of The Gardner Report, I suggested we would see more homes come to market and that has proven to be accurate. Given these factors, I am moving the needle a little toward buyers, but it remains a staunchly seller’s market.

About Matthew Gardner

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

2 to 3

Along the Front Range we have gone from two weeks of inventory to three weeks.

For much of the Spring, there was only two weeks of inventory on the market in most areas. Meaning, it would only take 14 days to sell all of the homes currently for sale.

Now, because the pace of sales has slightly slowed down and there is a bit more inventory, there is roughly three weeks.

We can actually measure inventory in number of days based on the pace of sales in July so far:

- Metro Denver = 23 Days

- Larimer County = 22 Days

- Weld County = 22 Days

This is obviously good news for buyers as they have better selection and slightly less competition.

Millennial Buyers

Millennials often get a bad rap. One of the myths about Millennials is that they don’t own homes and will be renters forever.

Not true! Especially on the Front Range of Colorado.

Based on research by our very own Chief Economist, Matthew Gardner, Millennials make up a significant percentage of all home buyers in Metro Denver and Colorado.

In Metro Denver, 50% of all buyers last year were in the Millennial demographic.

In Northern Colorado, the number is 41%.

It turns out that Millennials, as they move into their mid to late 30’s, see the value of home ownership and are at the point in their lives where it makes sense to own instead of rent.

5 Deal Breakers That Can Blindside Home Buyers

Purchasing a home can be a complex endeavor for even the most well-prepared home buyer. You’ve diligently saved for your down payment, followed the market, researched agents and now you are ready to make an offer on your dream home. Don’t let these 5 “Deal Breakers” come between you and your new home.

-

- Big Purchases on Credit. It is tempting to buy the furniture for your new home or a new car for the garage before the sale closes. Take care if you are making these purchases on credit. Large purchases on credit can have a major impact on your credit profile which effects your mortgage application. It’s a better plan to wait until after closing or pay cash for these transactions or you may be putting that furniture in a different living room than you originally picked them out for.

-

- Overpaying. Before your bank will approve your mortgage they will appraise the home you are purchasing. If they feel you are overpaying they are likely to decline your mortgage application. If you find yourself in this situation consult with your agent on renegotiating your offer to be more in line with the bank’s appraised value.

-

- Purchasing too close to Foreclosure. If you are making an offer on a house which is facing foreclosure be sure to have a closing date set before the foreclosure date. Have your agent work with the lender to structure closing before the house goes back to the bank and into foreclosure.

-

- IRS liens. You’ve heard the old saying “Death and Taxes”. Back taxes and liens can derail your attempts to get financing for a mortgage so be sure to have your books in order before filing your loan application.

-

- Comprehensive Loss Underwriting Exchange (CLUE). CLUE is a database of insurance claims for both people and property. Your home insurance rates are determined by the information about you and the property you plan to purchase which is contained in this report. Past claims for water damage, falling trees and even dog bites from present and past owners can multiply your insurance rates. Consult your agent about the CLUE report for your future home as soon as possible once your home purchase offer is accepted.

When purchasing a home there will be challenges which you can plan for and the unexpected hurdles. By educating yourself as a consumer and choosing a well trained real estate agent you can avoid many of the pitfalls of 21st century home ownership.

What about you? Tell us if you have had any “deal breaker” experiences.

When Buying a Short Sale Home is the Right Fit

Purchasing a home can feel overwhelming at times, but a short sale home offers a unique opportunity for a prospective buyer. A short sale occurs when a homeowner owes a lender more than their home is worth, and the lender agrees to let the owner sell the home and accept less than what is owed. Lenders may agree to a short sale because they believe it will net them more money than going forward with a lengthy and costly foreclosure process.

Short sales do differ in a number of ways from conventional home sales. Here are a few things to consider if you’re thinking about buying a short sale property.

- Short sale homes sell for less, but not significantly less than market value.

Buyers hoping to snap up a home for half the market value will be disappointed. The selling price for short sales averages about 10 percent less than for non-distressed properties. The bank is looking to recover as much of the value of the home as possible, so they will not accept offers that are significantly under market value. That said, with savings that can equal tens of thousands of dollars, a short sale is a great way to get more house for your money.

- Short sale properties are sold “as is”.

The lender will not be making repairs to the home. Any improvements that need to be made are most likely going to be the responsibility of the buyer. A savvy buyer’s agent/broker will get contractor bids for any necessary repairs and use those to help negotiate a lower sales price with the bank.

- A short sale will take longer than a conventional home sale.

Once you and the seller have mutual acceptance on an offer, you need to allow 60 to 90 days for the lender approval process. There are often long stretches when the offer is slowly winding its way through the bank’s system, so buyers need to be patient.

- If you have to sell your home first, a short sale is probably not the best fit.

Lenders generally will not take contingent offers on a short sale.

- A short sale is one real estate transaction that you shouldn’t attempt on your own.

Short sales are complicated transactions that involve a different process and significantly more paperwork than a standard real estate sale. An agent/broker that is unfamiliar with short sales can write an offer in such a way that they inadvertently cause their buyers to lose the deal. An experienced short sale agent/broker will protect your interest and help the process move forward smoothly.

The bottom line: As long as you can be patient, and are working with an agent/broker who understands the process, buying a short sale is a great way to purchase the house you want at a price you’ll love.