Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

This analysis of the Metro Denver and Northern Colorado real estate markets is provided by Windermere Real Estate Chief Economist Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact us.

ECONOMIC OVERVIEW

Colorado added 45,300 non-agricultural jobs over the past 12 months, a growth rate of 1.7%. Although that is a respectable number, employment growth has been trending lower in 2017 as the state reaches full employment. Within the metropolitan market areas included in this report, there was annual employment growth in all areas other than Grand Junction, where employment was modestly lower. There was solid growth in Greeley and Fort Collins, where annual job growth was measured at 4% and 2.7%, respectively.

In November, the unemployment rate in the state was a remarkably low 2.9%, down from 3% a year ago. The lowest reported unemployment rates were seen in Fort Collins and Boulder, where only 2.5% of the labor force was actively looking for work. The highest unemployment rate (3.7%) was in Grand Junction.

The state economy has been performing very well, which is why the wage growth over the past year has averaged a very solid 3.3%. I expect the labor market to remain tight and this will lead to wages rising at above-average rates through 2018.

HOME SALES ACTIVITY

- In the fourth quarter of 2017, there were 14,534 home sales—a drop of 2.0% compared to a year ago.

- Sales again rose the fastest in Boulder County, which saw sales grow 17.9% versus the third quarter of 2016. There were also reasonable increases in Weld and Larimer Counties. Sales fell in all other counties contained within this report because there is such a shortage of available homes for sale.

- As I discussed in my third quarter report, sales slowed due to the lack of homes for sale. The average number of homes for sale in the markets in this report is down by 8.2% from the fourth quarter of 2016.

- The takeaway is that sales growth has moderated due to the lack of homes for sale.

HOME PRICES

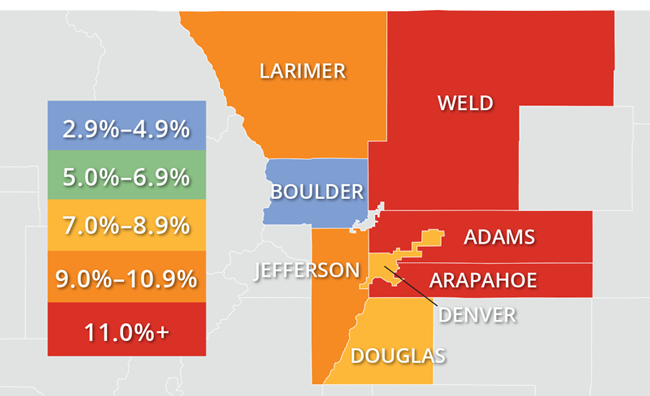

- With continued competition for the limited number of available homes, prices continued their upward trend. Average prices were up 9.8% year-over-year to a regional average of $431,403, which was slightly higher than the third quarter of 2017.

- There was slower appreciation in home values in Boulder County, but the trend is still positive.

- Appreciation was strongest in Weld County, which saw prices rise 14.3%. There were also solid gains in almost all other counties considered in this report.

- The ongoing imbalance between supply and demand persists, which means we can expect home prices to continue appreciating at above-average rates for the foreseeable future.

DAYS ON MARKET

- The average number of days it took to sell a home rose by two days when compared to the fourth quarter of 2016.

- Homes in all but three counties contained in this report took less than a month to sell. Adams County continues to stand out, where it took an average of just 21 days for homes to sell.

- It took an average of 29 days to sell a home last quarter. This is up nine days over the third quarter of 2017.

- Housing demand remains strong in Colorado and this will continue with well-positioned, well-priced homes continuing to sell very quickly.

CONCLUSIONS

This speedometer reflects the state of the region’s housing market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

For the fourth quarter of 2017, I have chosen to leave the needle where it was in the previous quarter. Listings remain scarce, but this did not deter buyers who are still active in the market. As much as I want to see more balance between supply and demand, I believe the market will remain supply-constrained as we move toward the spring, which will continue to heavily favor sellers.

Matthew Gardner is the Chief Economist for Windermere Real Estate, specializing in residential market analysis, commercial/industrial market analysis, financial analysis, and land use and regional economics. He is the former Principal of Gardner Economics, and has more than 30 years of professional experience both in the U.S. and U.K.