Facebook

Facebook

Twitter

Twitter

Pinterest

Pinterest

Copy Link

Copy Link

Quaint Home with Amazing Landscaping!

BEAUTIFULLY maintained home at 2509 Tulane Dr, just a block from O’Dea Elementary. Permitted addition makes this home almost 2,400 square feet. Wood floors on the main floor in fantastic condition, open kitchen to the living room. Newer style vinyl windows throughout, new roof in 2015, new carpet in most rooms, and a brand new furnace! Landscaping is as close to perfect as it can get. Large office, study and recreation room with its own access to the backyard. An amazing opportunity under $400,000 in South College Heights! Call Paul Hunter for a private showing or click the link below for more details.

https://windermerenoco.com/listing/77000317

A Look Back

Here are some fun facts about 2017…

(By the way, be sure to RSVP for our Market Forecast on January 18th so you can hear our predictions for next year. Click HERE to register)

In 2017:

- $4.6 billion of residential real estate was sold in Larimer and Weld Counties. ($2.8 in Larimer and $1.8 in Weld). This volume is double what is was in 2012.

- There were 7,091 residential sales in Larimer County and 5,442, in Weld County.

- On average, it took 53 days to sell a home in Larimer County and 49 days in Weld County. In 2012 it took about 25 days longer to sell a home.

Rate Recap

The Federal Reserve raised interest rates by 0.25% this week. It was their 3rd rate increase this year.

This has us thinking about mortgage rates.

Today, 30-year mortgage rates are 3.93%.

Inventory Is Up

For the past few years the hot topic in Northern Colorado real estate is

Housing Supply is an Issue that Will Not Improve Any Time Soon and Here’s Why

There are two common concerns about the housing market that one hears from both consumers and real estate professionals alike. First, they question whether or not we are on the brink of another housing bubble, and second, they want to know why there aren’t more homes for sale.

I don’t plan on addressing the concern regarding a housing bubble in this article except to say that we are not currently in “bubble” territory, although affordability does concern me immensely. Today I would like to concentrate on the second question about the lack of homes for sale.

According to the National Association of REALTORS®, there were 1.96 million homes for sale in the United States in May 2017. When adjusted for seasonality, this falls to just below 1.9 million which is essentially the same level we saw back in 2000.

Now consider that the country has added over 21 million new households during that same time period, and you can see why this is so troubling. It is worth noting that many of these new households did move into rental properties, but this still leaves the U.S. with a substantial housing shortfall, which explains why demand for homes is so high.

With the shortage of homes for sale, you would normally expect builders to meet this pent-up demand with new construction housing but, unfortunately, this has not been the case. In fact, new single-family housing starts are running at about 800,000 (annualized), and I believe we need starts to come in at over 1 million to satisfy demand – especially as older Millennials start to create households of their own and begin thinking about buying instead of renting.

We therefore have a quandary. Trust in the housing market has clearly returned, but there are not enough homes to meet the demand of buyers, and when a buyer does find a home, they are met with very stiff competition, which is driving prices increasingly higher.

So why are we in this position and how do we get out of it?

In reality, there is no single reason for the situation we are in today. Rather it is a number of factors that, when combined, suggest to me that the market will not return to equilibrium any time soon.

The first reason for the shortfall is purely demographic. As “Boomers” age, they are not following the trends of previous generations. Many are staying in the workforce far longer than their predecessors, and, as they are postponing retirement, they do not feel compelled to downsize. In fact, almost two-thirds of Boomers plan to age in place and not move even after retirement. Without this anticipated supply of homes from downsizing Boomers, there aren’t enough homes for move-up buyers, which in turn limits the supply of homes for first-time buyers.

Secondly, as a nation we just aren’t moving as often as we used to. When I analyze mobility, it is clear that people no longer have to relocate as frequently to find a job that matches their skill set. There has been a tangible drop in geographic specificity of occupations. Where we used to move to find work, this is no longer as prevalent, which means we are moving with less frequency.

Thirdly, as mentioned earlier, builders aren’t building as many homes as they could. This is essentially due to three factors: land supply/regulation, labor, and materials. The costs related to building a home have risen rapidly since the Great Recession, and this is holding many builders back from building to their potential. Furthermore, in order to justify the additional costs, many of the homes that are being built are larger and more expensive, and this is no help for the first-time buyer who simply can’t afford a new construction price tag.

Fourthly, while the general consensus is that home prices have recovered from the major correction that was seen following the recession, this is actually not the case in some markets. In fact, there are 32 U.S. metro areas where home prices are still more than 15 percent below the pre-recession peak. As equity levels remain low, or non-existent, in these markets, many would-be sellers are waiting until they have sufficient equity in their homes before putting them on the market.

And there is still one more issue that is certain to become a major factor over the next few years: interest rates.

Imagine, if you will, the country a few years from now when interest rates have normalized to levels somewhere around 6 percent. Now consider potential home sellers who are happily locked in at a mortgage rate of about 4 percent who are considering their options. Will they sell and lose the historically low rate that they currently have? Remember that for every 1 percent increase in rates, buyers can afford 10 percent less house. If they don’t HAVE to sell, their thoughts may lead to remodeling rather than moving. I think that this is a very reasonable hypothesis which could lead us to see low inventory levels for a lot longer than many think.

With little assistance from the new home market, I believe we will suffer from low inventory levels until well into 2018.

Our best hope for a more balanced market lies with builders, so hopefully they’ll be allowed to do what they do best – build more homes.

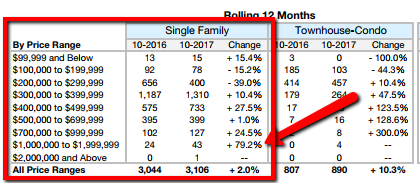

Limited Choices

Pretend that customer walks into our office and tells us they are looking for a single family home in Fort Collins. We would tell them that there  are 314 to choose from. But if they told us their price range is up to $300,000, their choices would be limited to just 10 homes.

are 314 to choose from. But if they told us their price range is up to $300,000, their choices would be limited to just 10 homes.

Our Crystal Ball

Last week Windermere’s Chief Economist Matthew Gardner joined us for our annual Market Forecast events in Colorado. We were pleased to host over 500 customers at two events in Denver and Fort Collins.

host over 500 customers at two events in Denver and Fort Collins.

Did You Know?

Here are some fun “Did You Know?” stats as we wrap up 2016 (arguably one of the most fascinating years in the history of Northern Colorado Real Estate)

Here are some fun “Did You Know?” stats as we wrap up 2016 (arguably one of the most fascinating years in the history of Northern Colorado Real Estate)

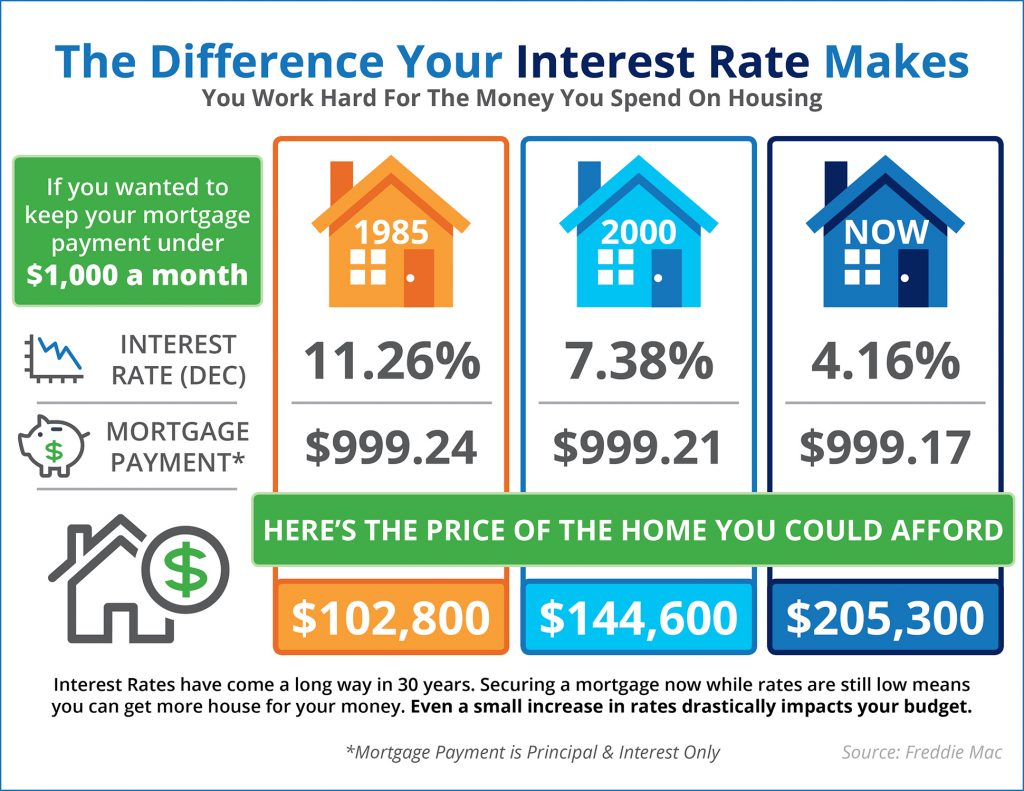

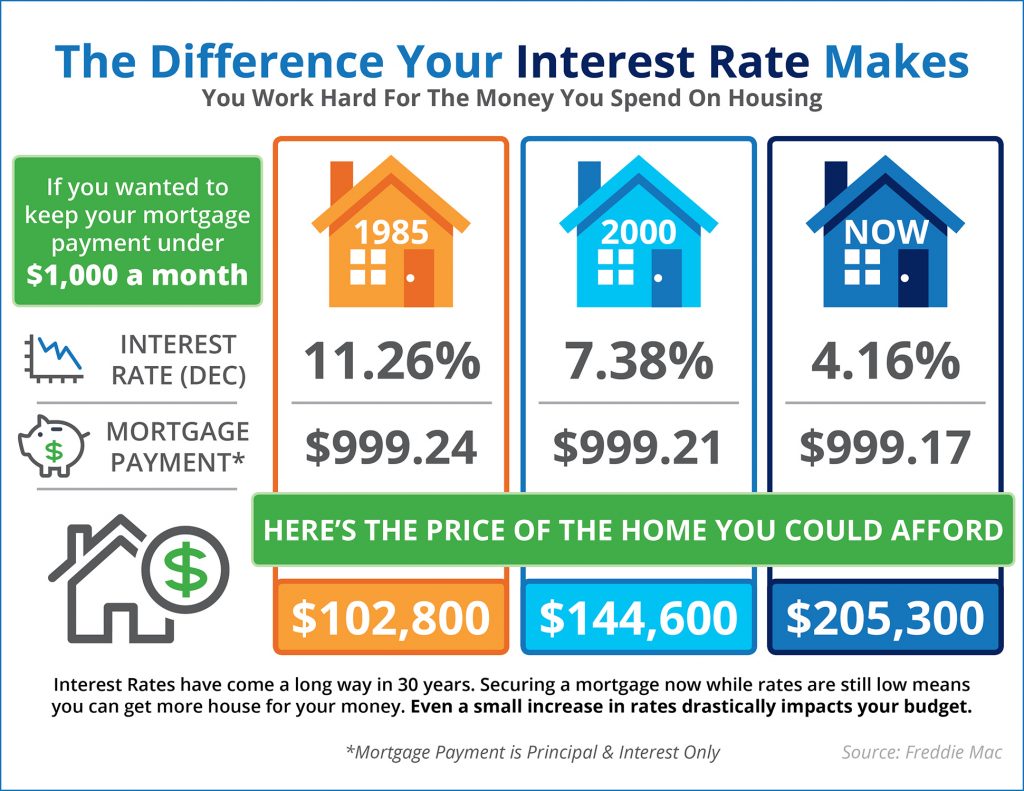

How Interest Rates Impact Your Buying Power

Know your risk. How will your buying power be impacted with increased interest rates?

Check out this infographic for an understanding of how much interest rates affect how much home you can afford.

Source: www.simplifyingthemarket.com Read the full article here: http://www.simplifyingthemarket.com/en/2016/12/16/the-impact-your-interest-rate-has-on-your-buying-power-infographic/?a=79696-9675764dc3b9cb63398c8d3c043b0717