Facebook

Facebook

Twitter

Twitter

Pinterest

Pinterest

Copy Link

Copy Link

The Risks and Rewards of Purchasing a Bank-Owned Home

The process of purchasing a home directly from a lender can be long and arduous, but could very well be worth it in the end. If you have your sights on a particular home or are looking to find a deal on your first, working directly with the lender may be your only option. Purchasing a bank-owned home is not for the faint of heart, here are some tips for negotiating the REO process:

1. Be prepared: The condition of bank-owned properties are often poor and hard to show. Past owners may have departed on bad terms, leaving the home in poor condition with foul smells, missing appliances, wires are taken from breakers, gas fireplaces gone, even bathrooms without toilets and sinks.

2. Understand the costs: Maintenance or repairs may be necessary since these homes have been vacant for an unknown period of time–sometimes months or years. Keep in mind, when they were occupied the owners could have been under financial hardship, preventing them from doing regular seasonal care or repairs when needed. Remember as well that the bank is trying to sell the house immediately, so you will receive a financial break in the price rather than a willingness to negotiate on the maintenance and repair issues.

3. Accept the unknown: In traditional real estate transactions, homeowners fill out Form 17 regarding important information about the history of the house. A bank-owned home is either exempt or marked with “I don’t know” throughout the document. Not having the accuracy of this 5-page disclosure form could leave you with a lot of unanswered questions on the history of the home.

4. Know what is non-negotiable: The pricing on the house may not get much lower. Some of these properties can be “a dream come true” if you get them at an amazing price, or they could be your worst nightmare. Do your due diligence researching any property, and conduct all necessary inspections to safeguard yourself. Some major repairs may be negotiable, but will likely not reduce the home price.

5. Make a clean offer: The higher the price you can offer, the better. Include your earnest money, keep contingencies to a minimum, and suggest a reasonable closing date. The simpler your offer is, the higher chance you have of the bank accepting your offer or countering in a reasonable time period.

6. Be patient: Consult with a professional who handles bank owned home purchases to help you negotiate the pathway to homeownership. The process of purchasing a bank-owned, foreclosed or short-sale home is typically longer than a typical real estate sale.

Limited Choices

Pretend that customer walks into our office and tells us they are looking for a single family home in Fort Collins. We would tell them that there  are 314 to choose from. But if they told us their price range is up to $300,000, their choices would be limited to just 10 homes.

are 314 to choose from. But if they told us their price range is up to $300,000, their choices would be limited to just 10 homes.

Our Crystal Ball

Last week Windermere’s Chief Economist Matthew Gardner joined us for our annual Market Forecast events in Colorado. We were pleased to host over 500 customers at two events in Denver and Fort Collins.

host over 500 customers at two events in Denver and Fort Collins.

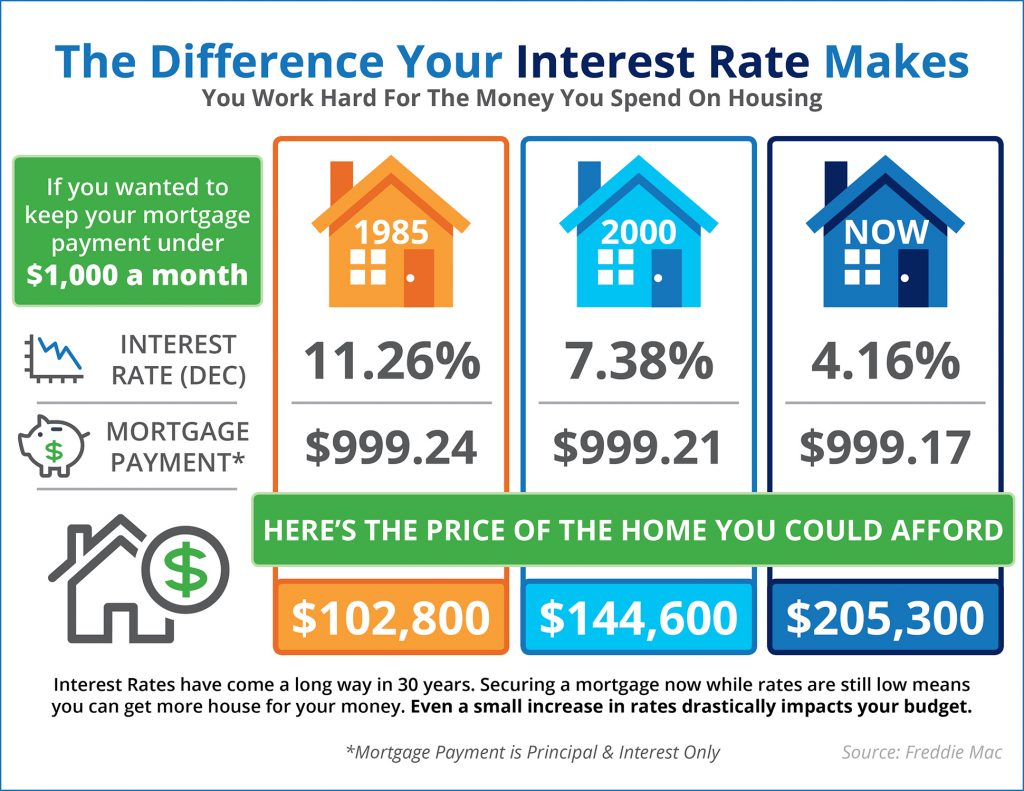

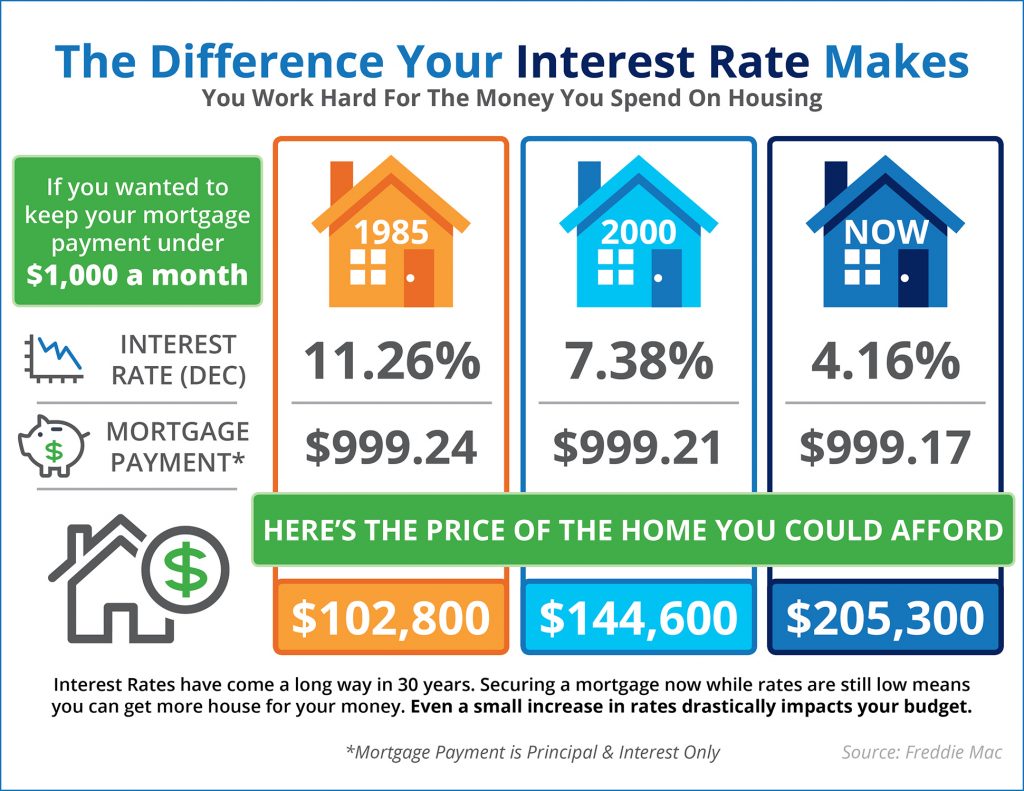

How Interest Rates Impact Your Buying Power

Know your risk. How will your buying power be impacted with increased interest rates?

Check out this infographic for an understanding of how much interest rates affect how much home you can afford.

Source: www.simplifyingthemarket.com Read the full article here: http://www.simplifyingthemarket.com/en/2016/12/16/the-impact-your-interest-rate-has-on-your-buying-power-infographic/?a=79696-9675764dc3b9cb63398c8d3c043b0717

100K

The City Manager for Fort Collins, Darin Atteberry, recently visited our weekly sales meeting. He had several interesting and valuable facts to share, including this…

Based on the City’s research, Fort Collins will grow by 100,000 people over the next 25 to 32 years. That will bring the population to approximately 255,000 people. It means Fort Collins will essentially add the equivalent of Boulder’s population over the next two and a half decades.

Based on the City’s research, Fort Collins will grow by 100,000 people over the next 25 to 32 years. That will bring the population to approximately 255,000 people. It means Fort Collins will essentially add the equivalent of Boulder’s population over the next two and a half decades.

The Trump Tantrum

Since the election interest rates have jumped from 3.77% to 3.95% according to the Mortgage Bankers Association.

Since the election interest rates have jumped from 3.77% to 3.95% according to the Mortgage Bankers Association.

“This week’s increase in mortgage rates, being dubbed the ‘Trump Tantrum,’ is the biggest one week increase since the ‘Taper Tantrum‘ in June 2013,” said Bankrate’s chief financial analyst Greg McBride.

Economists say the anticipation of Trump’s pledged spending plans and tax cuts have investors anticipating some inflation and a dose of adrenaline to the economy which have caused a great deal of volatility in the market.

A little perspective is in order- rates today are still lower than the 3.97% recorded last year at this time. And, rates today are still essentially half of their long-term average.

Using a $400,000 home as an example with a 20% down payment, this interest rate increase translates to an additional $34 per month.

Many economists believe that we are now seeing the beginning of a long-term rise in interest rates.

source: Inman News

Beware of Low Down Payments

First-time buyers can borrow with little down, but that may not be wise

Financial planners warn: "Borrowers should not overlook the true measure of home affordability: monthly cash flow."

Is your down payment going to affect your cash flow in the end? Check out this article to see what they suggest.

http://www.cnbc.com/2016/09/02/homebuyers-beware-of-banks-offering-too-much-cash.html