Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

From Renting To Owning

According to a report by Fannie Mae, 74% of consumers plan to buy a home the next time they move. This included 43% of consumers that are currently renting.

The interesting fact is that 9 out of 10 consumers overstated or didn’t know the minimum down payment required for most mortgage programs. The great news is that of those surveyed, 70% of the respondents said they were saving specifically for a down payment.

Speaking with a lender is the first step to understanding the current mortgage requirements. Reach out to your Windermere agent for great lender recommendations.

5 Deal Breakers That Can Blindside Home Buyers

Purchasing a home can be a complex endeavor for even the most well-prepared home buyer. You’ve diligently saved for your down payment, followed the market, researched agents and now you are ready to make an offer on your dream home. Don’t let these 5 “Deal Breakers” come between you and your new home.

-

- Big Purchases on Credit. It is tempting to buy the furniture for your new home or a new car for the garage before the sale closes. Take care if you are making these purchases on credit. Large purchases on credit can have a major impact on your credit profile which effects your mortgage application. It’s a better plan to wait until after closing or pay cash for these transactions or you may be putting that furniture in a different living room than you originally picked them out for.

-

- Overpaying. Before your bank will approve your mortgage they will appraise the home you are purchasing. If they feel you are overpaying they are likely to decline your mortgage application. If you find yourself in this situation consult with your agent on renegotiating your offer to be more in line with the bank’s appraised value.

-

- Purchasing too close to Foreclosure. If you are making an offer on a house which is facing foreclosure be sure to have a closing date set before the foreclosure date. Have your agent work with the lender to structure closing before the house goes back to the bank and into foreclosure.

-

- IRS liens. You’ve heard the old saying “Death and Taxes”. Back taxes and liens can derail your attempts to get financing for a mortgage so be sure to have your books in order before filing your loan application.

-

- Comprehensive Loss Underwriting Exchange (CLUE). CLUE is a database of insurance claims for both people and property. Your home insurance rates are determined by the information about you and the property you plan to purchase which is contained in this report. Past claims for water damage, falling trees and even dog bites from present and past owners can multiply your insurance rates. Consult your agent about the CLUE report for your future home as soon as possible once your home purchase offer is accepted.

When purchasing a home there will be challenges which you can plan for and the unexpected hurdles. By educating yourself as a consumer and choosing a well trained real estate agent you can avoid many of the pitfalls of 21st century home ownership.

What about you? Tell us if you have had any “deal breaker” experiences.

On Sale

With interest rates so low, one could argue that money is essentially on sale.

It’s actually half off.

30-year mortgage rates hit 3.75% which is exactly half of their long term average.

Rates have averaged 7.5% over the last 40 years so today buyers are getting half of that rate.

The “sale” on mortgage rates creates a significant savings in monthly payment because of the 1%/10% rule.

For every 1% change in interest rate, the monthly payment will change roughly 10%.

So when rates go up to 4.75%, a buyer’s payment will be 10% higher.

For example, the principal and interest payment on a $400,000 home with a 20% down payment at today’s rates is $1,482.

If rates were 1% higher, the payments jump up to $1,669.

Good Loan News

Here are two recently-announced pieces of really good news for home buyers.

• The Colorado Housing and Finance Authority recently raised the income limit for their down payment assistance program to $115,600.

Now more people can get help with a down payment.

• Fannie Mae and Freddie Mac raised their conforming loan limits so that more people can use a conforming loan and not be forced to use a ‘jumbo’ loan.

Contact us if you would like to hear how these pieces of news could help you.

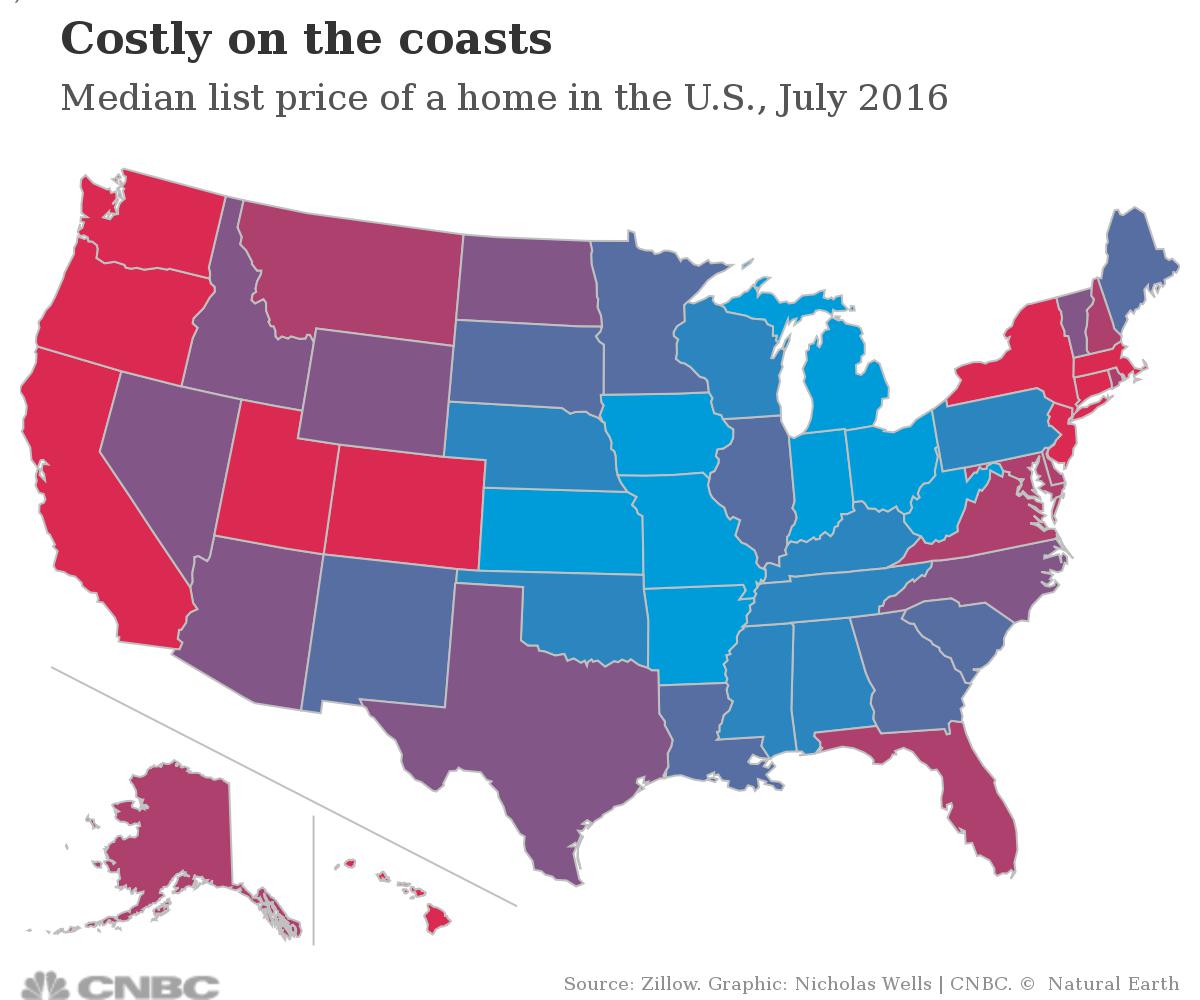

Limited Choices

Pretend that customer walks into our office and tells us they are looking for a single family home in Fort Collins. We would tell them that there  are 314 to choose from. But if they told us their price range is up to $300,000, their choices would be limited to just 10 homes.

are 314 to choose from. But if they told us their price range is up to $300,000, their choices would be limited to just 10 homes.

Our Crystal Ball

Last week Windermere’s Chief Economist Matthew Gardner joined us for our annual Market Forecast events in Colorado. We were pleased to host over 500 customers at two events in Denver and Fort Collins.

host over 500 customers at two events in Denver and Fort Collins.

100K

The City Manager for Fort Collins, Darin Atteberry, recently visited our weekly sales meeting. He had several interesting and valuable facts to share, including this…

Based on the City’s research, Fort Collins will grow by 100,000 people over the next 25 to 32 years. That will bring the population to approximately 255,000 people. It means Fort Collins will essentially add the equivalent of Boulder’s population over the next two and a half decades.

Based on the City’s research, Fort Collins will grow by 100,000 people over the next 25 to 32 years. That will bring the population to approximately 255,000 people. It means Fort Collins will essentially add the equivalent of Boulder’s population over the next two and a half decades.

The Trump Tantrum

Since the election interest rates have jumped from 3.77% to 3.95% according to the Mortgage Bankers Association.

Since the election interest rates have jumped from 3.77% to 3.95% according to the Mortgage Bankers Association.

“This week’s increase in mortgage rates, being dubbed the ‘Trump Tantrum,’ is the biggest one week increase since the ‘Taper Tantrum‘ in June 2013,” said Bankrate’s chief financial analyst Greg McBride.

Economists say the anticipation of Trump’s pledged spending plans and tax cuts have investors anticipating some inflation and a dose of adrenaline to the economy which have caused a great deal of volatility in the market.

A little perspective is in order- rates today are still lower than the 3.97% recorded last year at this time. And, rates today are still essentially half of their long-term average.

Using a $400,000 home as an example with a 20% down payment, this interest rate increase translates to an additional $34 per month.

Many economists believe that we are now seeing the beginning of a long-term rise in interest rates.

source: Inman News

Beware of Low Down Payments

First-time buyers can borrow with little down, but that may not be wise

Financial planners warn: "Borrowers should not overlook the true measure of home affordability: monthly cash flow."

Is your down payment going to affect your cash flow in the end? Check out this article to see what they suggest.

http://www.cnbc.com/2016/09/02/homebuyers-beware-of-banks-offering-too-much-cash.html